Japan's Long Comeback

Stocks around the world hit new all-time highs last week, but one stood out.

- The U.S. S&P 500 Index eclipsed the high set just the week before.

- Europe's STOXX 600 Index climbed above its prior high set a little over two years ago in January 2022.

- Japan's Nikkei 225 Index hit a new all-time high set 34 years ago.

We have been eagerly anticipating this move by Japan's stocks market, highlighted last June in Japan: Reclaiming Lost Decades. Today, the Nikkei 225 Index continues to outperform the S&P 500. Even though Japan's stock market is the second largest in the world, it often doesn't get much attention; the Nikkei 225 Index peaked in 1989 and had not hit a new all-time high until now. Japan's stocks are up 17% this year (the slide in the yen relative to the dollar this year reduced that gain to 10% when measured in US dollars), making it the best-performing market in the world in 2024 in either currency.

Japan's stock market climbs above prior high set in December 1989

Source: Charles Schwab, Macrobond data as of 2/23/2024.

Data indexed to 100 at the start of 1950. An index number is a figure reflecting price or quantity compared with a base value, which is assigned the index number of 100. The index number is expressed as 100 times the price or quantity ratio to its base value. Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested indirectly. Past performance is no guarantee of future results.

Japanese stocks have been outperforming the S&P 500 since the global bear market ended in October 2022. The Nikkei 225 posted a gain of 39.9% during the current bull market compared with 31.4% for the S&P 500, both measured in U.S. dollars from the end of October 2022 through the end of last week (February 23, 2024), as you can see in the chart below.

Japan's stocks have outperformed since the current bull market began

Source: Charles Schwab, Macrobond data as of 2/26/2024.

Data indexed to 100 at the start of 10/31/2022. An index number is a figure reflecting price or quantity compared with a base value, which is assigned the index number of 100. The index number is expressed as 100 times the price or quantity ratio to its base value. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

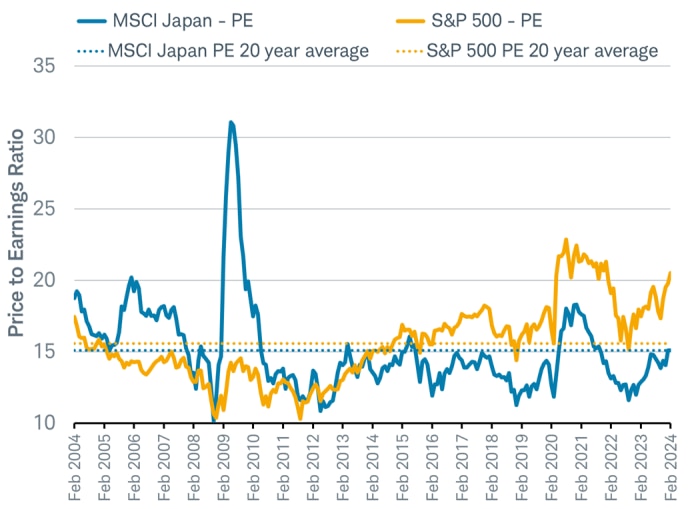

The outperformance by Japan's stock market may be surprising to some investors. Unlike the S&P 500, Japan's stock market doesn't have a handful of highly valued stocks pushing it to new highs. In fact, the forward price-to-earnings (PE) ratio for Japan's stock market is 15.1, in line with the 20-year average for the MSCI Japan Index. In comparison, the S&P 500 forward price-to-earnings ratio is 20.5, 32% above its 20-year average of 15.6.

Japan's stock market valuation in line with 20-year average

Source: Charles Schwab, FactSet data as of 2/24/2024.

Past performance is no guarantee of future results.

While some investors may be put off by Japan's sluggish economic growth in recent decades, it's important to remember that many Japanese companies like Sony and Toyota get 70%-80% of their sales outside of Japan according to their earnings reports, demonstrating how they are tied to global consumers more so than to domestic ones. That exposure has helped to propel earnings growth even as domestic economic growth has been weak. The return to the 1989 bubble peak for Japan's stock market is supported by much higher earnings per share than would be presumed by Japan's economic growth. Corporate profits for Japanese companies are now about three times what they were the last time stocks were at these levels. Earnings per share for Japanese companies in the MSCI Japan Index grew +8.3% in 2023, measured in U.S. dollars. This growth came despite Japan's economy slipping into a recession with back-to-back quarters of negative GDP growth in the third and fourth quarters of last year.

Japan's corporate profits have grown since stocks last peaked

Source: Charles Schwab, Macrobond, Japan Ministry of Finance as of 2/24/2024.

Past performance is no guarantee of future results.

Japan's earnings outlook may benefit from the global manufacturing recovery getting underway in 2024, as global demand for goods revives. The global manufacturing PMI climbed to 50.0 in January, reaching the threshold between expansion and contraction for the manufacturing sector. The preliminary February Purchasing Managers' Index (PMI) readings for the U.S., Germany, France, Japan, U.K., and other major countries were released last week. The February readings were mixed; some improved a little, some weakened slightly. The final global reading for February may come in around 50.0 again, helping confirm an end to the longest downturn in manufacturing since the data began 30 years ago (16 months). A related timely indicator of global manufacturing that we watch closely is signaling a similar trend. Demand for the cardboard boxes that manufactured goods tend go into is also reviving (measured by demand for corrugated fiberboard that most cardboard boxes are made out of). All this signals a recovery from what we termed the "cardboard box" recession of 2023 as we anticipated in our 2024 Outlook and may lift manufacturing-driven economies like Japan out of recession and support continued earnings growth.

"Cardboard Box" recovery

Source: Charles Schwab, Fibre Box Association, S&P Global, Bloomberg data as of 2/23/2024.

Support for Japan's stock market may come from the new savings program intended to encourage Japanese investors to move money from cash into stocks. This year's new NISA, or the Nippon Individual Savings Account, is a Japanese government tax-free stock investment program for individuals intended to promote households' investment in stocks. According to the Bank of Japan, only 13% of Japan's liquid household assets are in stocks versus over 40% in the U.S. and 21% in Europe, contrasting with cash deposits making up 52.5% of households' financial assets in Japan, 12.5% in the U.S. and 35.5% in the eurozone.

Potential re-allocation: household allocation to stocks and cash

Source: Charles Schwab, Bank of Japan data as of December 23, 2023.

Additional support for Japan's assets may come from the end of an era at the Bank of Japan (BOJ). For over a decade, the BOJ's policy of zero or negative interest rates has enabled Japan to be an important source of investment funding, with negative interest rates allowing investors to borrow cheaply in yen and then purchase investments in other countries offering a higher return. The BOJ is widely expected by the market and economists to hike rates by this June. Any rate hikes this year hold the potential to prompt Japanese investors to sell foreign assets and bring them home, incentivized by higher interest rates and the best performing stock market in the world so far in 2024.

Further gains by the second largest stock market in the world can help boost the performance of international stocks. Stocks headquartered in Japan make up 23% of the MSCI EAFE Index, the largest share of any country in the index. We believe Japan could continue to surprise many investors with strong performance driven by a confluence of positive factors. Yet, there are risks.

- Japan's aging population. Japan's aging population had tended to restrain domestic growth and inflation, although Japan has some unique advantages in combating this drag relative to other countries. First, unlike many developed economies where the domestic population is the largest customer base, more than half of the sales of Japanese companies are outside of Japan mitigating this risk. Second, the potential wave of capital spending could boost output per worker in Japan, whose productivity is among the lowest of the G7. Third, the costs of an aging population are much less of a drag for Japan than the United States. Japan is aging more quickly than the U.S., but health care costs per capita for Japan ($4,378 during pre-pandemic 2019 according to the World Bank) are a fraction of those in the U.S. ($12,914 during pre-pandemic 2019), per the U.S. Centers for Medicare & Medicaid Services.

- Japanese stocks have seen a powerful rally already. Strong net money inflows and double-digit gains so far this year have pushed Japan's stocks to an all-time high.

- Ultimately, Japan's debt growth may be unsustainable. As of December 2023, Japan's government debt is 255% of GDP, double that of the U.S. (123%), and the highest of any developed nation according to the International Monetary Fund (IMF). To help finance this debt, the Bank of Japan has bought half (54%) of all Japanese government bonds, known as JGBs—double the share of U.S. government debt owned by the U.S. Federal Reserve (20%). This large growth in debt financed with low interest rates has weighed on the value of Japan's currency. The yen has fallen over 30% against the dollar since the end of 2020, when the bank's self-imposed ceiling on purchasing JGBs was lifted in response to the pandemic. This effect on its currency may eventually act as a market-imposed debt limit for Japan. However, since Japan has a high savings rate and can finance its debt without relying on foreign investment, it is not clear how high the domestically financed government debt can grow without adverse effect.

Japan's stock market may continue to surprise investors as it sets new all-time highs. However, the uniqueness of Japan's economy and businesses also pose risks.