Federal Reserve: On the Road Again

Federal Reserve Chair Jay Powell often employs driving metaphors when talking about how he sees monetary policy. In 2022, he described setting interest rate policy as "driving down a foggy road"—going slowly, to avoid running off the road. More recently, he indicated that the "direction of travel is clear" for interest rates to move lower. However, the pace and magnitude of rate cuts are still to be determined by economic conditions.

The bond market is pricing in the potential for the Fed to take the express lane to much lower interest rates, despite the Fed's hesitancy in this cycle. Barring a recession, we expect the Fed to maintain a more measured pace. Fast or slow, the important message for investors is that the central bank is exiting its tight policy stance. All roads lead to lower interest rates.

A fork in the road?

In the last six months, conditions have developed that allow the Fed to ease policy. Inflation has fallen, and the labor market has cooled. These satisfy the criteria for the Fed's dual mandate to maintain price stability while aiming for full employment. The inflation metric that the Fed favors in setting policy, the personal consumption expenditures index excluding food and energy prices, or "core PCE," has fallen by half, from a peak year-over-year rate of 5.2% in 2022 to 2.6%.

Core PCE has fallen by half from its 2022 peak

Source: Bloomberg.

PCE: Personal Consumption Expenditures Price Index (PCE DEFY Index), Core PCE: Personal Consumption Expenditures: All Items Less Food & Energy (PCE CYOY Index), percent change, year over year. Monthly data as of 7/31/2024.

Moreover, the leading indicators of inflation are pointing to further declines. Wholesale prices for raw materials such as energy and industrial metals are falling sharply as global demand slows. China's economic slump has led to a broader slowdown that has spread to Europe and some emerging-market countries. While U.S. gross domestic product (GDP) growth has remained firm in the 2.5% to 3.0% region, global growth is pulling inflation lower.

Wholesale prices have declined sharply from their 2022 peak

Source: U.S. Bureau of Labor Statistics.

U.S. Producer Price Index Final Demand, U.S. Producer Price Index Final Demand Less Foods Energy and Trade Services, Percent Change from Year Ago, Monthly, Seasonally Adjusted. Data as of 8/31/2024.

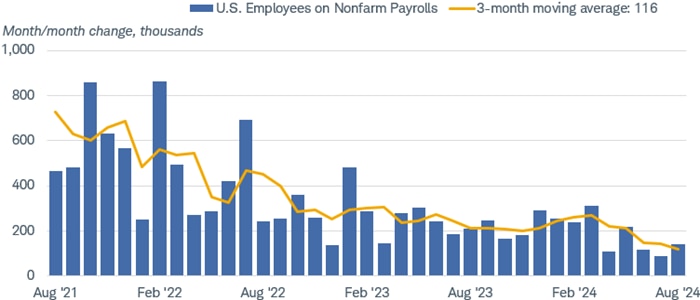

A slowdown in employment growth is another factor propelling the Fed toward easing. The pace of job growth has slowed substantially, and the unemployment rate has risen since last year. A rising unemployment rate is a key indicator for the Fed in setting policy. At 4.2% the overall unemployment rate is still low, but the increase from 3.4% is a worrying sign that the economic conditions are deteriorating.

U.S. employment growth has slowed

Source: Bloomberg.

US Employees on Nonfarm Payrolls Total MoM Net Change SA (NFP TCH Index). Monthly data as of 8/31/2024.

Will the Fed take the express lane?

With a rate cut at the September 17-18 Federal Open Market Committee (FOMC) meeting a foregone conclusion, the question now is, "How quickly will the Fed move?" The target range for the policy rate—the federal funds rate, which is the rate banks charge each other for overnight loans—is currently set at 5.25% to 5.5% with inflation near 2.5%, leaving plenty of room for the Fed to lower rates.

Inflation is significantly lower than the federal funds target rate

Source: Bloomberg.

Federal Funds Target Rate - Upper Bound (FDTR Index), U.S. Personal Consumption Expenditure Core Price Index YOY SA (PCE CYOY Index). Monthly data as of 08/31/2024.

Shaded areas indicate past recessions.

We would argue that the Fed could start the cycle by cutting the fed funds rate by 50 basis points (or 0.5%) and then moderating the speed depending on conditions. However, in past cycles, the Fed has cut rapidly when the economy was in recession or in crisis, such as the pandemic. A fast cycle might be defined as when the Fed cuts five times in a year's time. That has only happened in recessionary or crisis periods. Currently, the economy is not in recession or crisis, but the Fed is trying to avoid a recession. In cycles when the Fed is cutting in response to falling inflation, the pace has been moderate.

The pace of rate cuts historically has varied

Source: Bloomberg U.S. Aggregate Bond Index, as of 8/30/2024.

The chart shows the six-month and 12-month total return of the Bloomberg U.S. Aggregate Bond Index after the first rate cut in each of the 12 cycles. For the 6- and 12-month forward total returns, month-end data was used. Total returns for the rate cutting periods beginning on 11/1970, 11/19/1971, and 12/9/1974, are unavailable due to index limitations. Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

Direction more important than speed

While the pace matters, it's the direction of travel that is most important for investors. Bond yields are falling and are likely to continue to move lower as the rate-cutting cycle begins. Based on the current structure of the Treasury yield curve, we see more room for short-term rates to fall than long-term rates. The yield spread between two-year Treasuries and 10-year Treasuries has recently moved from steeply inverted to slightly positive.

The yield curve has moved from inverted to slightly positive

Source: Bloomberg.

Market Matrix US Sell 2 Year & Buy 10 Year Bond Yield Spread (USCY2Y10 INDEX). Data as of 9/9/2024.

The rates are comprised of Market Matrix U.S. Generic spread rates (USYC2Y10). This spread is a calculated Bloomberg yield spread that replicates selling the current 2-year U.S. Treasury Note and buying the current 10-year U.S. Treasury Note, then factoring the differences by 100. Shading indicates past recessions. Past performance is no guarantee of future results.

While we continue to suggest that investors with a high allocation to cash or short-term bonds should consider extending duration, we would look beyond the Treasury market to do so. We look at the Bloomberg U.S. Aggregate Bond Index as a benchmark. It has a current yield-to-worst (the lowest possible return on a bond with an early-retirement provision, barring default) of 4.2% and a duration of 6.1 years. For most investors, a duration in that region would allow for capturing attractive yields over an intermediate time frame while mitigating volatility.

But we favor staying in higher-credit-quality bonds for the majority of a portfolio. Investment-grade corporate bonds and government agency bonds currently offer yields in the 4.5% region with durations of about six to seven years, which is about 75 to 100 basis points higher than Treasury yields of similar duration.

In addition, investment-grade municipal bonds can offer attractive tax-equivalent yields for investors in high tax brackets. For investors willing to take more risk, a small allocation to preferred securities could make sense, but volatility is likely to be high.

Yields on various bonds may offer more than Treasuries of similar duration

Source: Bloomberg, as of 9/6/2024.

Indexes represented are: Bloomberg U.S. Aggregate Bond Index (U.S. Aggregate), Bloomberg U.S. Corporate Bond Index (IG Corporates), Bloomberg U.S. Corporate High-Yield Bond Index (HY Corporates), Bloomberg U.S. Municipal Bond Index (Municipal Bonds), ICE BofA Fixed Rate Preferred Securities Index (Preferreds), Bloomberg Emerging Market USD Aggregate Index (EM USD Bonds), Bloomberg U.S. MBS Index (MBS), Bloomberg U.S. Treasury Index (Treasuries), and the S&P 500 Dividend Aristocrats Index (Dividend Aristocrats). Yields shown are the average yield-to-worst except for the Dividend Aristocrats which is the average dividend yield. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

All roads appear to lead to lower rates

With the Federal Reserve and most major central banks in easing mode and treasury yields well above the inflation rate, the direction of travel for rates appears lower. Despite the strong bond market rally over the past few months, we still see room for yields to fall further. This road trip isn't over yet.